“

”Markets in Focus

Timely analysis of market moves and sectors of opportunity

The Fed kept its policy rate unchanged at its latest Federal Open Market Committee meeting, while showcasing its easing bias.

With the possibility of a potential hike effectively off the table, investors should expect rates to remain high — not higher — for longer while the Fed closely monitors incoming inflation and jobs data.

As earnings and key macro data releases slow, equities can grind higher with a few “catalyst-light” months ahead.

Following three stronger than expected Consumer Price Index (CPI) prints and elevated Employment Cost Index (ECI) data on the last day of April, markets went into the Federal Open Market Committee (FOMC) meeting worried about a hawkish pivot.

That’s not what happened.

“The May FOMC meeting leaned dovish, and we should breathe a sigh of relief that rates will simply remain high, not higher, for a while longer,” said Matt Orton, CFA, Chief Market Strategist at Raymond James Investment Management.

The FOMC kept rates unchanged for a sixth straight meeting and, despite persistently high inflation readings to start the year, Fed Chair Jerome Powell’s comments confirmed an easing bias and essentially closed the door on a rate hike. While the Fed noted the lack of further progress on inflation, it maintained references to a future reduction of interest rates in its statement. This message was also emphasized during the press conference with mention that reducing policy restraint too late or too little could unduly weaken the economy and jobs market, and suggested that the bias to ease rates remains.

The Fed also announced that tapered balance sheet runoff will begin on June 1, with a slightly larger cut than expected to the runoff caps in the United States Treasury System Open Market Account (SOMA). Those caps will go from $60 billion/month to $25 billion/month.

Orton stressed that with hikes essentially off the table for now, it reaffirms his view that rate cuts should be viewed as when they will happen, not if. When Powell was asked whether the committee would be satisfied with inflation remaining around a 3% pace for the rest of the year, he again guided to the notion that the committee believes that the existing level of rates will be enough to get inflation down. “Of course we’re not satisfied with 3% inflation,” Powell said. “We think our policy stance is appropriate to achieve (2% inflation). The policy focus has really been on holding the current level of restriction. That’s where the discussion was focused.”

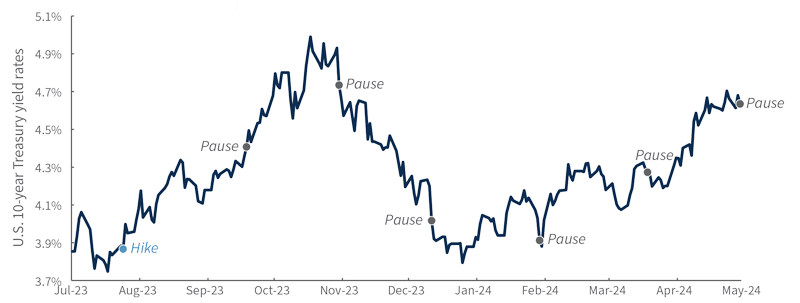

Fed holds policy rate steady for 6th consecutive meeting

U.S. 10-year Treasury yield since July 2023

Source: Bloomberg, as of 5/1/2024

Orton believes the bar to cut has gotten higher since the March meeting, and he doesn’t think even a significant surprise would put June or July back on the table for rate cuts. “December is my base case for one cut in 2024,” Orton said.

Economic alarmists also received a dose of humor and realism when Powell answered a question about the potential for stagflation by responding, “I don’t see the ‘stag’ or the ‘flation.’”

The market reaction through the early part of FOMC post-meeting communications was dovish, with implied rates and the U.S. dollar pulling back.1 Equities jumped while U. S. Treasuries gained on the statement’s lack of a more hawkish twist to forward guidance, as well as a surprisingly large cutback in quantitative tightening.

Orton didn’t like the sharp reversal in equities to close May 1 with the S&P 500 Index reversing a +1.4% move with no clear catalyst, but he said it was encouraging to see green the following morning.

“We still have the payrolls report the morning of May 3 but, hopefully, the context of the FOMC meeting will allow markets to take a strong print in stride. We should want a strong economy to support earnings growth,” Orton said. He suspects that once we get past this week, with earnings and key macro data releases slowing a bit, that equities can grind higher with a few “catalyst-light” months, and shared that election years also typically see a summer lull in volatility.

“At this point, I feel more comfortable deploying capital on market weakness, particularly to cyclical parts of the market and taking advantage of generationally attractive yields,” Orton said. He also wants to ensure it’s top of mind that sticky inflation tends to correspond to stronger-for-longer pricing power for corporations, and that better corporate profitability tends to lead to higher capital expenditures — noting that between just four of the largest mega-caps there’s nearly $200 billion being invested in the next year alone. And, he cautioned not to forget about structural tailwinds for capital expenditures such as supply chain reshoring, providing the electric needs for data center buildouts, and more.

Small-cap stocks outperformed May 1 after posting their worst monthly performance since September, with the Russell 2000® Index down 7.04%. If investors take the rate hike scenario off the table, small-cap stocks could benefit, and Orton said the entry point is interesting if you believe we’re nearing the trough in earnings. The Russell 2000® Index has lagged the S&P 500 Index by nearly 8% year to date and sits nearly 20% below its 2021 all-time high. Quality has worked well down the market capitalization spectrum and, so far, Orton said it’s been a strong year for active small-cap stock managers across styles.

“Again, this highlights the importance of being active down market capitalization,” he said, “and I believe investors who don’t have exposure to — or are underweight — small-cap stocks should consider adding some to their investment mix following this FOMC meeting.”

1 Unless otherwise indicated, all data cited is sourced from Bloomberg as of May 1, 2024.

Risk Information:

Investing involves risk, including risk of loss.

Diversification does not ensure a profit or guarantee against loss.

Disclosures:

Index or benchmark performance presented in this document does not reflect the deduction of advisory fees, transaction charges, or other expenses, which would reduce performance. Indexes are unmanaged. It is not possible to invest directly in an index. Any investor who attempts to mimic the performance of an index would incur fees and expenses that would reduce return.

This document is a general communication being provided for informational purposes only. It is educational in nature and not designed to be taken as advice or a recommendation for any specific investment product, strategy, plan feature, or other purpose in any jurisdiction, nor is it a commitment from Raymond James Investment Management or any of its affiliates to participate in any of the transactions mentioned herein. Any examples used are generic, hypothetical, and for illustration purposes only. This material does not contain sufficient information to support an investment decision, and you should not rely on it in evaluating the merits of investing in any securities or products. In addition, users should make an independent assessment of the legal, regulatory, tax, credit, and accounting implications and make their own determinations together with their own professionals in those fields. Any forecasts, figures, opinions, or investment techniques and strategies set out are for information purposes only, based on certain assumptions and current market conditions, and are subject to change without prior notice. All information presented herein is considered to be accurate at the time of production, but no warranty of accuracy is given and no liability in respect of any error or omission is accepted. It should be noted that investment involves risks, the value of investments and the income from them may fluctuate in accordance with market conditions and taxation agreements, and investors may not get back the full amount invested. Both past performance and yields are not reliable indicators of current and future results.

The views and opinions expressed are not necessarily those of the broker/dealer or any affiliates. Nothing discussed or suggested should be construed as permission to supersede or circumvent any broker/dealer policies, procedures, rules, and guidelines.

Sector investments are companies engaged in business related to a specific sector. They are subject to fierce competition and their products and services may be subject to rapid obsolescence. There are additional risks associated with investing in an individual sector, including limited diversification.

Investing in small cap stocks generally involves greater risks, and therefore, may not be appropriate for every investor. The prices of small company stocks may be subject to more volatility than those of large company stocks.

International investing presents specific risks, such as currency fluctuations, differences in financial accounting standards, and potential political and economic instability. These risks are further accentuated in emerging market countries where risks can also include possible economic dependency on revenues from particular commodities or on international aid or development assistance, currency transfer restrictions, and liquidity risks related to lower trading volumes.

Definitions

Capital expenditures, or capex, are monies used by a company to buy, improve, or maintain physical assets such as real estate, facilities, technology, or equipment, and may include new projects or investments.

The U.S. Consumer Price Index (CPI) measures the change in prices paid by consumers for goods and services. The U.S. Bureau of Labor Statistics bases the index on prices of food, clothing, shelter, fuels, transportation, doctors’ and dentists’ services, drugs, and other goods and services that people buy for day-to-day living. Prices are collected each month in 75 urban areas across the country from about 6,000 households and 22,000 retailers.

Cyclical stocks have prices influenced by macroeconomic changes in the economy and are known for following the economy as it cycles through expansion, peak, recession, and recovery.

The federal funds rate, known as the fed funds rate, is the target interest rate set by the Federal Open Market Committee of the U.S. Federal Reserve. The target is the Fed’s suggested rate for commercial banks to borrow and lend their excess reserves to each other overnight.

The Employment Cost Index measures the change in the cost of labor, free from the influence of employment shifts among occupations and industries, for three- and 12-month periods. The U.S. Bureau of Labor Statistics collects data for the index from thousands of private and government employers nationwide.

The Federal Open Market Committee (FOMC) consists of 12 members: the seven members of the Board of Governors of the Federal Reserve System; the president of the Federal Reserve Bank of New York; and four of the remaining 11 Reserve Bank presidents, who serve one-year terms on a rotating basis. The FOMC holds eight regularly scheduled meetings per year at which it reviews economic and financial conditions, determines the appropriate stance of monetary policy, and assesses the risks to its long-run goals of price stability and sustainable economic growth.

The Federal Reserve’s balance sheet is a statement of the assets and liabilities of the U.S. central bank. It shows what the Fed owns, mainly U.S. Treasury securities and mortgage-backed securities, and what it owes, mainly U.S. currency and reserve deposits of other financial institutions. The Fed’s balance sheet reflects its monetary policy and its influence on the money supply and interest rates in the economy.

Guidance refers statements from the managers of publicly traded companies that indicate whether they expect to realize near-term profits or losses and why.

Hawkish, dovish, and centrist are terms used to describe the monetary policy preferences of central bankers and others. Hawks prioritize controlling inflation and may favor raising interest rates to reduce it or keep it in check. Doves tend to support maintaining lower interest rates, often in support of stimulating job growth and the economy more generally. Centrists tend to occupy the middle of the continuum between tight (hawkish) and loose (dovish) monetary policy.

Market capitalization, or market cap, refers to the total dollar market value of a company’s outstanding shares of stock.

A market-implied policy rate is an estimate of the policy rate that reflects the difference between the current policy rate and an estimated forward or futures rate.

Mega-cap stocks are the largest publicly traded companies as measured by market capitalization. Generally, this refers to companies with market capitalizations over $200 billion.

The payroll report, officially known as the Employment Situation Summary, is a monthly U.S. Bureau of Labor Statistics (BLS) report tracking nonfarm payroll employment and the national unemployment rate, with data on changes in average hourly earnings, and job trends in public and private sectors of employment. The report is based on surveys of households and employers.

A policy rate is an interest rate set by a central bank or other monetary authority to influence the evolution of an economy’s monetary variables such as consumer prices, exchange rates, or credit expansion.

Quantitative tightening, also known as quantitative tapering, refers to the attempt by central bankers to reverse the effects of quantitative easing (QE), which is a form of unconventional monetary policy in which a central bank purchases longer-term securities from the open market in order to increase the money supply and encourage lending and investment. In quantitative easing, buying securities adds new money to the economy, and also serves to lower interest rates by bidding up fixed-income securities. It also expands the central bank’s balance sheet. In quantitative tightening, reducing those purchases is a policy primarily aimed at interest rates and at influencing investor perceptions of the future direction of interest rates.

Stagflation, first described after the oil shocks of the 1970s, is an economic condition that includes slow economic growth (or even declines in gross domestic product), relatively high unemployment, and inflation.

Tailwind is a term used to describe events or market forces that exert a positive influence on an investment’s performance. The opposite of a tailwind is a headwind, which contributes to an investment’s underperformance.

The System Open Market Account (SOMA) is managed by the Federal Reserve Bank. It contains domestic securities and foreign currency portfolios of the Federal Reserve, which are acquired through operations in the open market and serve as a management tool, liquidity resource for emergency events, and as collateral for liabilities on the Federal Reserve’s balance sheet.

Indices

The S&P 500 Index measures change in stock market conditions based on the average performance of 500 widely held common stocks. It is a market-weighted index calculated on a total return basis with dividend reinvested. The S&P 500 represents approximately 80% of the investable U.S. equity market.

The Russell 2000® Index measures the performance of the 2,000 smallest companies in the Russell 3000® Index, which represents approximately 7% of the total market capitalization of the Russell 3000® Index.

London Stock Exchange Group plc and its group undertakings (collectively, the “LSE Group”). ©LSE Group 2024. FTSE Russell is a trading name of certain of the LSE Group companies. Russell® is a trademark of the relevant LSE Group companies and is used by any other LSE Group company under license. All rights in the FTSE Russell indexes or data vest in the relevant LSE Group company which owns the index or the data. Neither LSE Group nor its licensors accept any liability for any errors or omissions in the indexes or data and no party may rely on any indexes or data contained in this communication. No further distribution of data from the LSE Group is permitted without the relevant LSE Group company’s express written consent. The LSE Group does not promote, sponsor, or endorse the content of this communication.

M-541006 Exp. 9/5/2024